Accounting Principles: Accounting Principles refer to the fundamental concepts and guidelines that govern the practice of financial accounting. These principles provide standardization and consistency in recording, reporting, and analyzing financial data, ensuring accuracy and reliability in financial statements.

Bookkeeping Fundamentals: Bookkeeping Fundamentals encompass the basic principles and techniques used to record financial transactions accurately and systematically. It involves tasks such as maintaining ledgers, reconciling accounts, and preparing financial statements, providing a solid foundation for effective financial analysis and decision-making.

Expertise with Excel: Expertise with Excel includes proficiency in using spreadsheet software to analyze financial data and perform various calculations. It allows financial analysts to efficiently organize data, create models, generate charts and graphs, and apply advanced functions to facilitate data analysis and reporting.

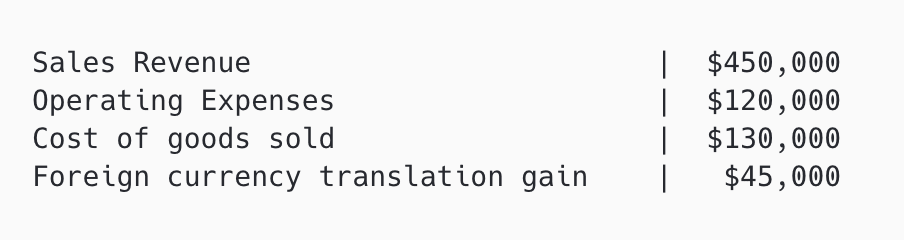

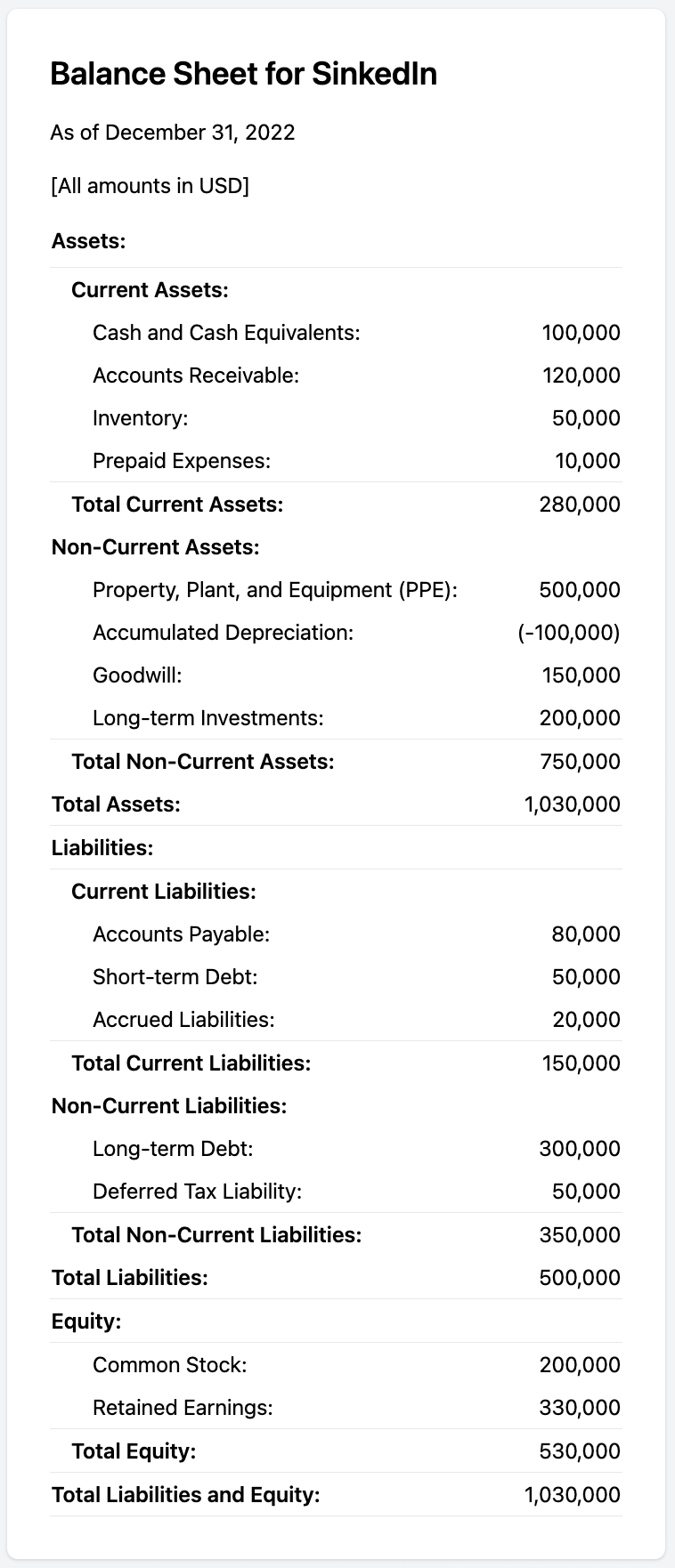

Financial Statements: Financial Statements are formal reports that provide a summary of a company's financial transactions, performance, and position during a specific period. The analysis of financial statements allows financial analysts to assess a company's profitability, liquidity, and solvency, providing valuable insights for evaluating its financial health and making informed decisions.

Budgeting and Forecasting: Budgeting and Forecasting involve the process of planning and estimating future financial outcomes based on historical data, market trends, and strategic objectives. It enables financial analysts to develop budgets, set financial targets, and project potential financial scenarios, helping organizations allocate resources effectively and make informed business decisions.

Financial Ratios: Financial Ratios are mathematical indicators that measure and evaluate the relationships between different elements of a company's financial statements. They provide insights into a company's liquidity, profitability, efficiency, and solvency, allowing financial analysts to assess its financial performance, identify trends, and compare it to industry benchmarks.

Investment Analysis: Investment Analysis involves evaluating the financial viability and potential risks and rewards of investment opportunities. It enables financial analysts to assess the value of investments, estimate future returns, and evaluate the risk factors associated with different investment options, providing guidance for making investment decisions that align with organizational goals and risk appetite.

Risk Management: Risk Management refers to the identification, assessment, and mitigation of potential risks that may negatively impact a company's financial performance and objectives. Financial analysts use risk management techniques and tools to assess risks, develop risk mitigation strategies, and ensure the effective allocation of resources to minimize potential losses and safeguard the organization's financial stability.

Cost of Capital: Cost of Capital represents the required rate of return that a company must achieve on its investments to maintain the value of its capital. It includes the cost of debt and equity financing and serves as a benchmark for evaluating investment projects and determining the optimal capital structure. Financial analysts measure the cost of capital to assess the feasibility and profitability of investment opportunities.

Capital Budgeting: Capital Budgeting involves the process of evaluating and selecting long-term investment projects, such as purchasing new equipment or expanding operations. Financial analysts apply various techniques, such as net present value (NPV) and internal rate of return (IRR), to assess the profitability, cash flow implications, and potential risks associated with capital investment decisions.